|

Getting your Trinity Audio player ready...

|

By: Abe Wertenheim

There are moments in a city’s economic life when the data becomes too stark to ignore, when the lived reality of residents collides so forcefully with policy ambitions that even the most entrenched narratives must be reconsidered. Manhattan’s rental market has reached precisely such a moment.

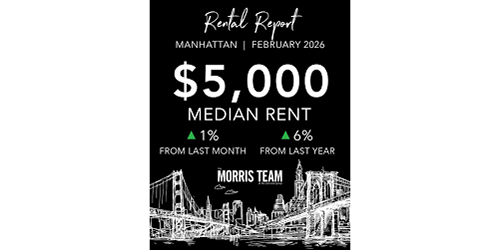

With median rent surging to an unprecedented $5,000, as reported on Saturday by The New York Post, the city now finds itself confronting a crisis that is both deeply structural and profoundly human. Behind the headline figure lies a convergence of policy decisions, economic pressures, and unintended consequences that have transformed what was once a difficult housing market into something approaching a full-scale affordability emergency.

Yet, perhaps most concerning is not the severity of the crisis itself, but the persistence of policy responses that risk exacerbating rather than alleviating the problem. Chief among these is the renewed push for rent freezes—an idea that, while intuitively appealing, threatens to deepen the very conditions it seeks to remedy.

The numbers, as detailed by The New York Post, are sobering. A median rent of $5,000 represents not merely a statistical milestone but a psychological threshold, a point at which the cost of living in Manhattan begins to feel unattainable for even upper-middle-income earners.

This figure marks a 6 percent increase from the previous year, outpacing broader inflation and underscoring the unique pressures facing the housing market. At the same time, inventory has contracted sharply. Corcoran reports just 5,290 active listings in February—a 26 percent decline compared to the same period a year earlier.

With a vacancy rate hovering at a mere 2 percent, the market is effectively gridlocked. In such an environment, prices are not merely rising; they are accelerating, driven by a scarcity that leaves prospective tenants with few viable alternatives.

As one real estate professional told The New York Post, “Nothing’s going to pop up, and the prices will keep increasing over time.” This is not hyperbole; it is a reflection of fundamental supply constraints that no amount of rhetorical optimism can overcome.

It is tempting to attribute rising rents solely to external factors such as inflation or population growth. Yet the evidence suggests that policy decisions have played a central role in shaping the current landscape.

Legislation such as the Housing Stability and Protection Act and the Fairness in Apartment Rental Expenses law were introduced with the explicit aim of protecting tenants. However, as The New York Post has reported, these measures have produced outcomes that diverge sharply from their intended goals.

The Housing Stability and Protection Act, for instance, imposed strict limitations on landlords’ ability to increase rents or recover costs associated with renovations. While this may have provided short-term relief for some tenants, it has also reduced the incentive for property owners to invest in or even maintain certain units.

As Gary Malin of Corcoran explained to The New York Post, many apartments that could theoretically enter the market remain unavailable because owners cannot justify the cost of bringing them up to code. The result is a hidden inventory—a pool of housing that exists in theory but not in practice.

Similarly, the FARE Act, which shifted the burden of broker fees from tenants to landlords, has had the unintended effect of embedding those costs into rent itself. Rather than eliminating expenses, the policy has simply redistributed them in a way that raises overall prices.

These examples illustrate a broader principle: when policies fail to account for the economic behavior of market participants, they often produce counterproductive outcomes.